Taxi fares for graveyard-shift BPO agents in Metro Manila run PHP 300 to 500 per trip. Two trips a day, five or six days a week, and a starting agent can burn through PHP 6,000 to 10,000 monthly on transportation alone. That’s 15% to 25% of take-home pay disappearing before rent, food, or savings ever enter the picture. If you’re running an e-commerce operation with a Philippine support or fulfillment team, this financial reality shapes your retention numbers more than any employee engagement survey will tell you. The mechanism behind BPO employee financial planning is worth understanding because it explains why some teams stay stable for years while others churn through agents every quarter.

The Night-Shift Cost Trap

E-commerce customer support, order processing, and live chat coverage for US and Australian storefronts typically require Philippine agents to work between 9 PM and 6 AM local time. This isn’t a minor inconvenience. It restructures an employee’s entire cost of living.

Public transit in Metro Manila shuts down or becomes unsafe after 10 PM. So agents take taxis, ride-hailing services, or company shuttles. The ones without company shuttles pay out of pocket. Food options shift too. Cooking at home becomes impractical when you sleep during the day and work at night. Convenience store meals, fast food near the office, and 24-hour eateries replace home-cooked food, adding PHP 3,000 to 5,000 monthly in food cost premiums over a daytime worker’s budget.

Health costs creep up over time. Chronic sleep disruption leads to more frequent doctor visits, vitamin supplements, and energy drinks that become a daily line item. None of these expenses show up in a job description, but they reduce the effective value of a BPO salary by 25% to 40% compared to an equivalent daytime role.

This is why attrition in night-shift BPO roles runs higher than daytime positions even when the base salary is identical. The mechanism is straightforward: the job costs more to hold than it appears on paper.

How Semi-Monthly Pay Cycles Shape Cash Flow

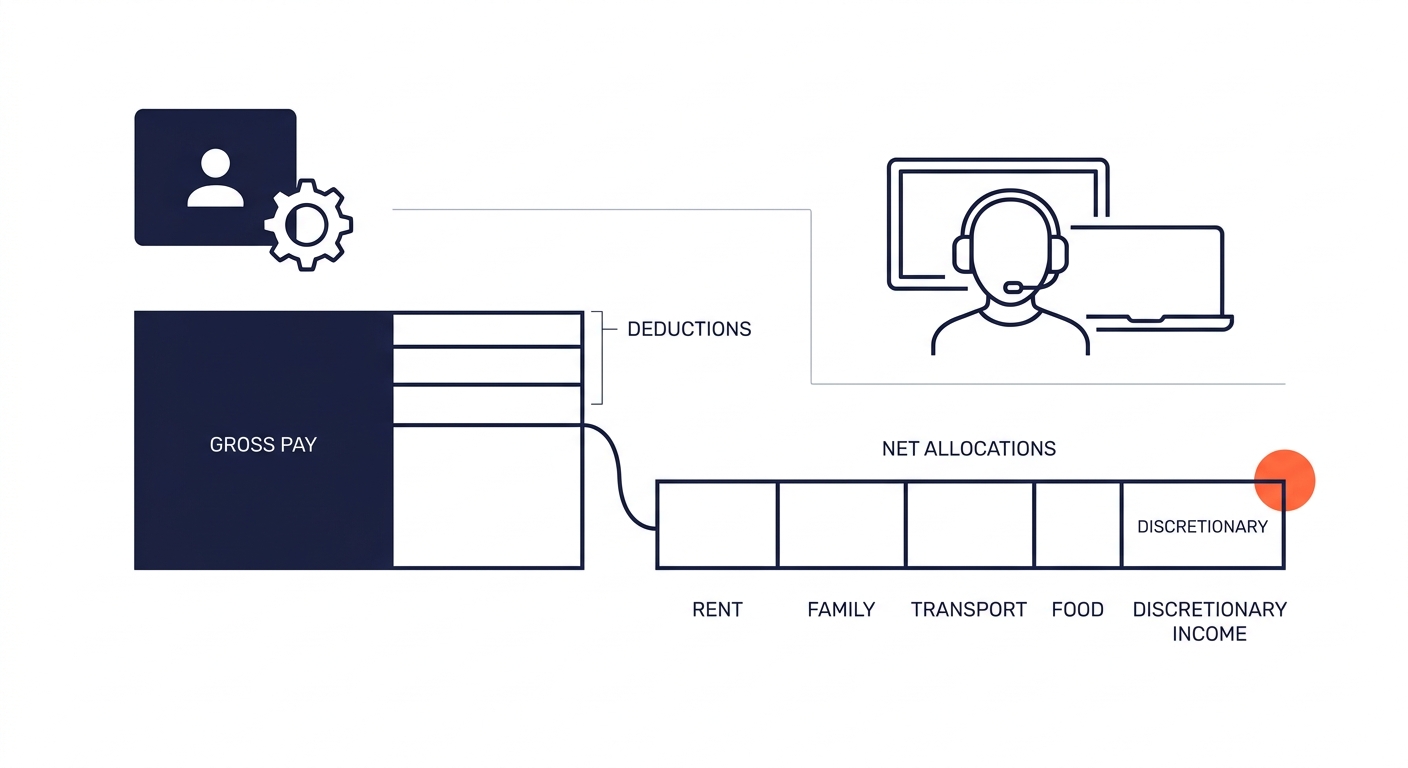

Philippine labor law requires employers to pay workers at least twice per month, with no more than 16 days between paydays. Most BPO companies pay on the 15th and 30th. This creates a predictable cash flow pattern that, paradoxically, makes financial planning harder for lower-income employees.

Here’s why. Mandatory deductions come out of each paycheck: SSS (Social Security System) contributions, PhilHealth (national health insurance), and Pag-IBIG (the Home Development Mutual Fund). These are non-negotiable and employer-matched. On a PHP 20,000 monthly salary, mandatory deductions reduce take-home pay by roughly PHP 1,500 to 2,000. Add withholding tax for employees earning above the threshold, and the first paycheck of the month often covers rent and utilities with almost nothing left. The second paycheck covers everything else: food, transportation, loan payments, and family support.

The family support piece is critical and often invisible to foreign employers. In the Philippines, it’s culturally expected for working adults to contribute financially to parents, siblings in school, or extended family. BPO agents commonly send 10% to 30% of their pay to family members each month. This isn’t optional spending in any practical sense.

So the actual discretionary income for a starting BPO agent earning PHP 18,000 to 25,000 monthly is often PHP 2,000 to 5,000. That’s the entire pool available for savings, emergencies, or investment. Financial planning at this income level requires precision, and the margin for error is razor-thin.

The Automation Fix

The single most effective financial planning mechanism for Philippine BPO employees is automated savings deductions. Financial advisor Randell Tiongson puts it directly: automate your savings and investments, because relying on willpower with a PHP 3,000 discretionary budget doesn’t work.

The mechanics look like this. On payday, before the employee touches their bank app, a standing instruction moves a fixed amount into a separate savings account or investment vehicle. The amounts are small by Western standards. PHP 500 to PHP 2,000 per paycheck. But consistency at these amounts compounds into meaningful sums over two to three years.

Several BPO companies in the Philippines have begun integrating financial wellness programs that set up automatic Pag-IBIG MP2 contributions (a voluntary savings program with a historically higher dividend rate than commercial bank savings accounts) or payroll-deducted mutual fund contributions. These programs work because they remove the decision point from every pay cycle. The employee opts in once, and the mechanism runs without requiring ongoing discipline.

Financial planning at BPO salary levels isn’t about picking the right stock or timing the market. It’s about engineering cash flow so that savings happen before spending does.

For e-commerce operators who manage their own offshore teams, understanding this mechanism matters for practical reasons. If your Philippine outsourced bookkeeping or customer support team has access to payroll-integrated savings programs, they’re less likely to face the kind of financial emergencies that cause absenteeism and sudden resignations. Some BPO operators now treat financial wellness programming as a retention tool with measurable ROI, reducing annualized attrition by 5 to 12 percentage points.

Investment Vehicles Philippine Workers Actually Use

Once the savings automation is running, the question becomes where the money goes. Philippine BPO employees typically have access to four categories of investment vehicles, each with different risk and liquidity profiles.

Pag-IBIG MP2 is the entry point for most. It’s a voluntary savings program run by the government’s Home Development Mutual Fund. Dividends have historically ranged from 5% to 7% annually, which beats inflation and most bank savings rates. Minimum contribution is PHP 500 per month. The lock-up period is five years, which discourages early withdrawal.

UITFs (Unit Investment Trust Funds) are offered by major Philippine banks. They pool investor money into managed portfolios. Entry points start at PHP 1,000 to PHP 10,000 depending on the bank and fund type. Bond funds are popular among conservative BPO savers; equity funds attract those with longer time horizons.

Mutual Funds through companies like Sun Life, BPI Investment Management, and others operate similarly to UITFs but are managed by non-bank investment companies. Some BPO companies partner with these firms to offer payroll-deducted contributions.

Stock market accounts through the Philippine Stock Exchange are accessible with as little as PHP 5,000 to open, but adoption among entry-level BPO employees remains low. The learning curve is steeper, and the volatility is harder to stomach when your total invested capital is small.

For employees who need shorter-term financing for emergencies or major purchases, options like SSS salary loans or Pag-IBIG multi-purpose loans provide below-market interest rates. Those exploring broader lending options can find where to get a loan through comparison platforms that aggregate offers from banks and alternative lenders.

The pattern across all of these: the mechanism works when contributions are automatic, amounts are fixed, and the employee doesn’t need to make active decisions each pay period. The moment it requires monthly manual action, participation drops off sharply.

How This Connects to Your E-Commerce Staffing Model

If you run an e-commerce business that relies on outsourced data entry teams, customer service agents, or an accounting virtual assistant based in the Philippines, the financial planning landscape of your team directly affects your operational stability.

An agent dealing with a cash emergency is more likely to take an unscheduled absence, accept a competing offer for a PHP 2,000 monthly bump, or lose focus during a shift. Across a 10-person support team, even one or two financially stressed employees can create enough coverage gaps to affect your customer response times and order processing accuracy.

Companies that have addressed common outsourcing mistakes around team retention often find that compensation structure matters more than compensation amount. A PHP 22,000 salary with automated savings, a company shuttle, and a meal allowance can retain better than a PHP 25,000 salary with none of those structural supports. The effective financial position of the employee is stronger in the first scenario, even though the number on the payslip is lower.

This applies to BPO providers you contract with, too. When evaluating an outsourcing partner for your e-commerce operations, asking about employee financial wellness programs and average tenure gives you a proxy for operational stability that sales decks won’t surface on their own. The Philippine call center industry’s rapid growth means agents have options, and the providers who retain talent are usually the ones engineering financial stability into their compensation design.

Where the Model Breaks

Automated savings and investment access are real mechanisms with documented outcomes. They work. But they operate within constraints that limit their impact for a large portion of the BPO workforce.

The first constraint is starting salary. At PHP 15,000 to 18,000 per month, which remains common for entry-level voice agents, the math doesn’t leave room for meaningful savings after mandatory deductions, night-shift costs, and family obligations. Automation can’t create surplus where none exists. For agents at this income level, the most impactful financial intervention is a pay increase or a cost reduction (like a company shuttle), not a savings app.

The second constraint is financial literacy. Many BPO employees enter the workforce at 19 to 22 years old, often with limited exposure to investment concepts. Without structured onboarding into financial planning, the default behavior is to spend what arrives. The automation mechanism works when someone sets it up, but getting to that setup requires education and trust-building that many employers skip.

The third constraint is the informal economy around BPO clusters. Lending apps, salary advance services, and informal lending circles are pervasive in areas with high BPO employment. These can trap employees in cycles of borrowing against future paychecks, which undermines any savings mechanism running in parallel. An employee automating PHP 1,000 per paycheck into Pag-IBIG MP2 while carrying PHP 15,000 in lending app debt at 3% monthly interest is going backward.

The mechanism of BPO financial planning is sound at the structural level. Automate first, invest consistently, reduce night-shift costs where possible. But it functions best for employees already earning above the survival threshold, and it requires employer participation to reach those who aren’t there yet. For e-commerce operators building long-term offshore teams, recognizing these limits helps you design compensation packages that actually produce the retention and performance outcomes you’re paying for.